If you file an Employee Retirement Income Security Act (“ERISA”) long term disability lawsuit, your success will depend heavily on which legal standard of review the court applies. The standards are anything but equal. The one used in your case can have a substantial impact on your success.

The Two Standards of Review Courts May Apply

Within the Second Circuit (including New York), there are two standards that federal courts use to review the decisions of insurers in ERISA long term disability lawsuits: (1) a “de novo” standard; and (2) an “arbitrary and capricious” standard (also known as an “abuse of discretion” standard).

A De Novo Standard: Making it Easier to Overturn the Adverse Decision

The default standard of review is de novo. The de novo standard of review generally makes it easier to overturn your insurer’s decision in ERISA long term disability lawsuits. De novo literally means “anew.” Under a de novo standard, the court decides all issues in your case “anew.”

When applying the de novo standard of review in the Second Circuit, the court stands in the shoes of your insurer. The insurer’s previous determination is not taken into account. The court evaluates the evidence with a fresh set of eyes and decides whether you are disabled under the terms of your plan.

The de novo standard of review means the court will give no deference to any prior determinations made by your insurer. Because the court conducts a new and impartial review of your claim, this standard usually gives you the “fairest shake” in court.

An Arbitrary and Capricious Standard: Making it Difficult to Overturn the Adverse Decision

Although de novo is the default standard, the court may apply a more stringent standard called “arbitrary and capricious” review if the administrator demonstrates that it was effectively granted discretionary authority. This standard is sometimes referred to as an “abuse of discretion” standard. The arbitrary and capricious standard of review tends to favor the insurer and make it more difficult to overturn their decision.

Under the arbitrary and capricious standard of review, the court does not make a new decision about your claim with “fresh eyes.” Rather, the court reviews the administrator’s decision and only overturns it if it was “unreasonable” – that is, if the decision was an abuse of the insurer’s discretion. If the court uses an arbitrary and capricious standard of review, you may have a taller hill to climb to prove the insurer’s decision was incorrect.

How the Court Will Determine Which Standard to Apply

How do courts decide which standard of review to apply to your ERISA long term disability lawsuit? To answer this question, the court must apply an analysis involving several steps.

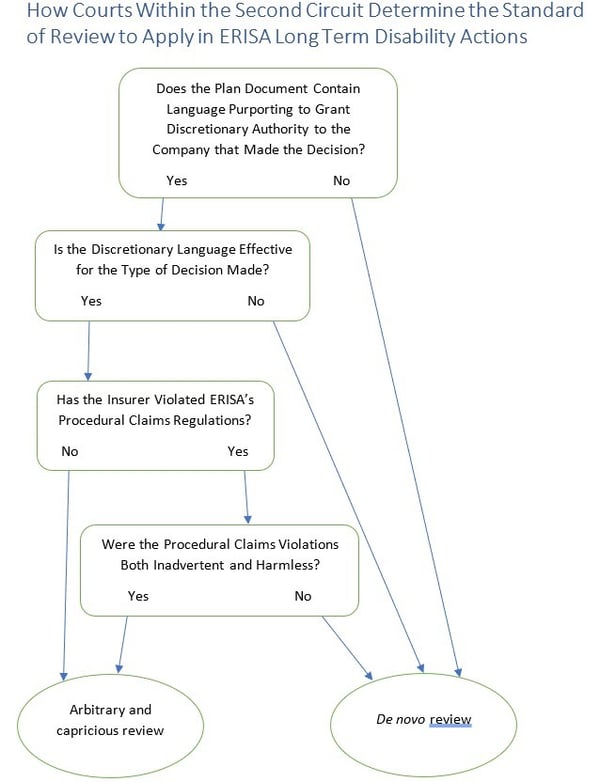

Does the Plan Document Contain Language Purporting to Grant Discretionary Authority to the Plan Administrator?

The court will first look to whether your long term disability insurance plan contains language purporting to grant discretionary authority to the plan administrator. In ERISA cases, the plan administrator is usually the insurer you are suing.

If no discretionary language is found in the plan document, the court will end its analysis and apply the more plaintiff-friendly de novo standard. If discretionary language is arguably found in the plan document, the court will move to the next step.

Did the Entity that Made the Adverse Determination Have Discretion?

The court may then consider whether the entity that made the final decision had discretionary authority. Just because the plan grants discretion to the plan administrator does not mean that the decision-making entity had discretion. Indeed, the decision-making entity is often not the same as the plan administrator.

For example, the discretionary language may explicitly grant discretion to Entity X, but Entity Y made the final decision at issue. Unless the plan permitted Entity X to delegate its discretionary authority to Entity Y, Entity Y made its decision without the benefit of discretion. The court’s analysis should end, and de novo review will apply.

If the decision-making entity was, in fact, delegated discretion by the plan document, the court will move to the next step.

Is the Discretionary Language Effective for the Type of Decision Made?

The court will then look to see whether the plan grants discretion to the decision-maker for the type of decision that it made.

For example, a plan may grant discretion to both determine eligibility for benefits and to interpret the terms of the plan. However, another plan may only grant discretion to determine eligibility for benefits. Another may only grant discretion to interpret plan terms.

The type of decision made must be compared to the type of authority that the plan grants. If the decision at issue falls outside the scope of the discretion granted, then the analysis ends with the court applying a de novo review standard. If the decision at issue falls within the scope of discretion set forth, the court will continue its analysis onto the next step.

Did the Decision-maker Forfeit Its Discretionary Authority by Violating ERISA’s Procedural Claims Regulations?

In the Second Circuit, including district courts in New York, the decision-maker can forfeit its discretionary authority by violating ERISA’s procedural claims regulations. Indeed, even if the plan effectively grants discretion, the court will still conduct a de novo review if: (1) the decision-maker failed to comply with ERISA’s procedural claims regulations; and (2) its claims violations were neither inadvertent nor harmless. Halo v. Yale Health Plan, 819 F.3d 42 (2nd Cir. 2016).

Under Halo, types of procedural claims violations that may trigger de novo review include failure to:

-

- Establish reasonable claim procedures. 29 C.F.R. § 2560.503-1(b); Easter v. Cayuga Med. Ctr. at Ithaca Prepaid Health Plan, 217 F. Supp. 3d 608 (N.D.N.Y. 2016).

- Give the claimant a chance to respond to a medical examination report. Hughes v. Hartford Life & Accident Ins. Co., 2019 U.S. Dist. LEXIS 49005 (D. Conn. March 25, 2019).

- Specify the reasons for a denial or termination. Cohen v. Liberty Mut. Group, 2019 U.S. Dist. LEXIS 55953 (S.D.N.Y. Mar. 31, 2019).

- Specify the policy provisions on which the decision is based. Montefiore Med. Ctr. v. Local 272 Welfare Fund, 2019 U.S. Dist. LEXIS 140293 (S.D.N.Y. Aug. 16, 2019).

- Provide an explanation of the scientific or clinical judgment for the decision. Tedesco v. I.B.E.W. Local 1249 Ins. Fund, 2017 U.S. Dist. LEXIS 133080 (S.D.N.Y. Aug. 21, 2017).

- Consider all evidence submitted by a claimant. Aitken v. Aetna Life Ins. Co., 2018 U.S. Dist. LEXIS 164008 (S.D.N.Y. September 25, 2018).

- Specify the insurer’s internal appeal procedures and time limits. McFarlane v. First Unum Life Ins. Co., 274 F. Supp. 3d 150 (S.D.N.Y. August 15, 2017).

- Provide an internal appeal that gives no deference to the initial claim decision. Schuman v. Aetna Life Ins. Co., 2017 U.S. Dist. LEXIS 39388 (D. Conn. March 20, 2017).

- Decide an initial application in a timely manner. Easter v. Cayuga Med. Ctr. at Ithaca Prepaid Health Plan, 217 F. Supp. 3d 608 (N.D.N.Y. 2016).

- Decide an administrative appeal in a timely manner. Spears v. Liberty Life Assur. Co. of Boston, 2019 U.S. Dist. LEXIS 169156 (D. Conn. Sept. 30, 2019).

If the insurer has committed any of these or other ERISA violations, de novo review should apply unless the insurer demonstrates that its violation was both inadvertent and harmless.

Helpful Analysis Flowchart

Conclusion

The standard of review the court applies in your ERISA long term disability lawsuit will have a significant effect on your chances of success. The experienced ERISA attorneys at Riemer Hess know how to make sure the court gets it right. We’ve been litigating these cases in the heart of New York City for over 25 years. Contact us to discuss the best strategy for your ERISA long term disability lawsuit.